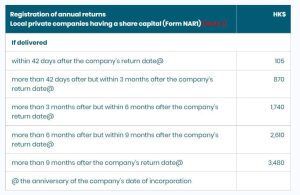

Hong Kong “Share Transfer” Stamp Duty Calculation (Applicable to Hong Kong Limited Company Shares Only)

- Tax rate and calculation basis

– Tax rate**: 0.2 %(買賣雙方各付0.1%, for a total tax rate of 0.2% of the transaction amount).

– Tax basis: whichever is higher of the “actual consideration” or “market value of shares” of the shares.

- Gratuitous transfer (gift)

– If there is no consideration for the transfer (e.g. a gift from a relative), stamp duty will still be calculated based on the market value of the shares.

– However, exemption may be made in some cases (supporting documents such as statutory declarations are required).

Key Details & Exemptions:

- Scope of application

– Only applicable to the transfer of shares in a Hong Kong registered limited company.

- Exemption conditions

– Internal Organisation: An exemption may be applied for for a qualifying intra-group transfer under Part XIVA of the Companies Ordinance.

– Relative transfers: Evidence of no business purpose (e.g., distribution of family assets) is required, but may still be subject to market value.

- Declaration and payment

– Instrument of Transfer** and tax must be paid within 30 days of the transfer.

– Late fines: up to 10 times the tax.

Process:

- Assess the value of shares

– Refer to the company’s net assets, recent transaction history, or professional valuation reports.

- Make a file

– Use of Contract Notes (usually handled by a secretarial company, in some cases by a solicitor).

- Pay stamp duty

– Obtain a stamp certificate through the website of the Inland Revenue Department of Hong Kong or in person.

- Complete the transfer

– Submit the stamped document to the Companies Registry for updating the register of members.

Inland Revenue Department (IRD) https://www.gov.hk/tc/residents/taxes/etax/services/share_transfer_computation.htm